Perhaps budgeting is second only to dieting on the “Least Motivating Activities” list. Budgeting, especially for a family sounds boring, daunting, and Humans are creatures of habit. Our brains love habits because they allow us to move to auto-pilot, freeing up our brain to focus on different things. Habits automate behaviors, turning difficult tasks into routine motions. So how can you turn your budget into a habit? Let’s first talk about how to change your behavior so that you establish the habit of budgeting.

Perhaps budgeting is second only to dieting on the “Least Motivating Activities” list. Budgeting, especially for a family sounds boring, daunting, and Humans are creatures of habit. Our brains love habits because they allow us to move to auto-pilot, freeing up our brain to focus on different things. Habits automate behaviors, turning difficult tasks into routine motions. So how can you turn your budget into a habit? Let’s first talk about how to change your behavior so that you establish the habit of budgeting.

Stanford University Professor BJ Fogg has developed a behavior model that looks at three elements needed to change behavior: motivation, ability, and triggers.

Motivation for budgeting is rooted in our need for order and control. A budget gives you an understanding of an important aspect of your life that should be within your control. You are probably looking to start a budget now because you need a loan or want to prepare for retirement. Perhaps your motivation is to save up to buy a home or to pay down your debt. All are motivators. These motivations boil down to hope, fear, and desire for acceptance. We’ll leverage this motivation for acceptance to help drive desired behaviors.

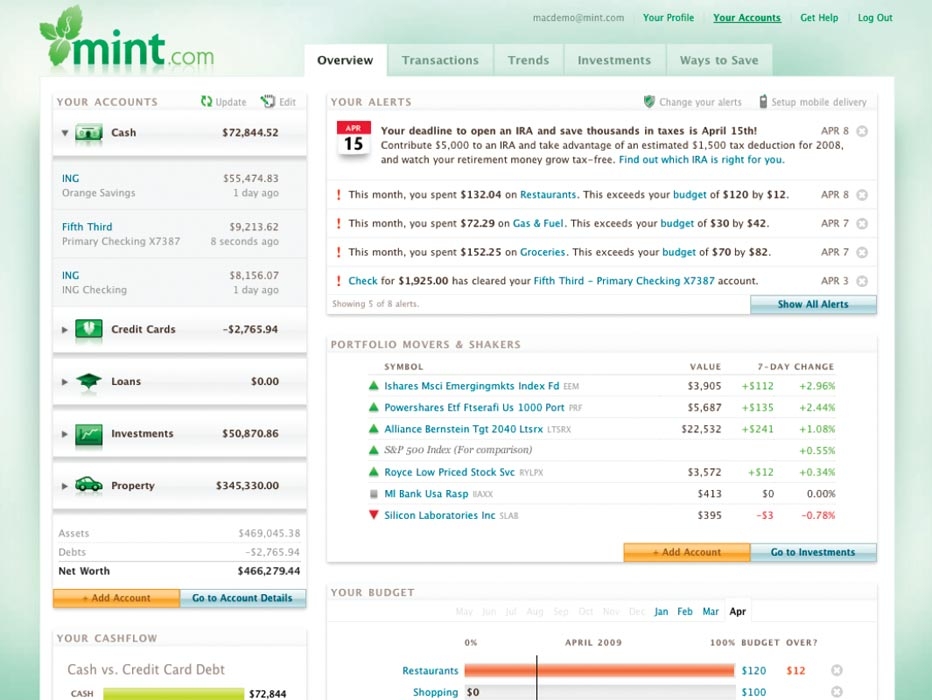

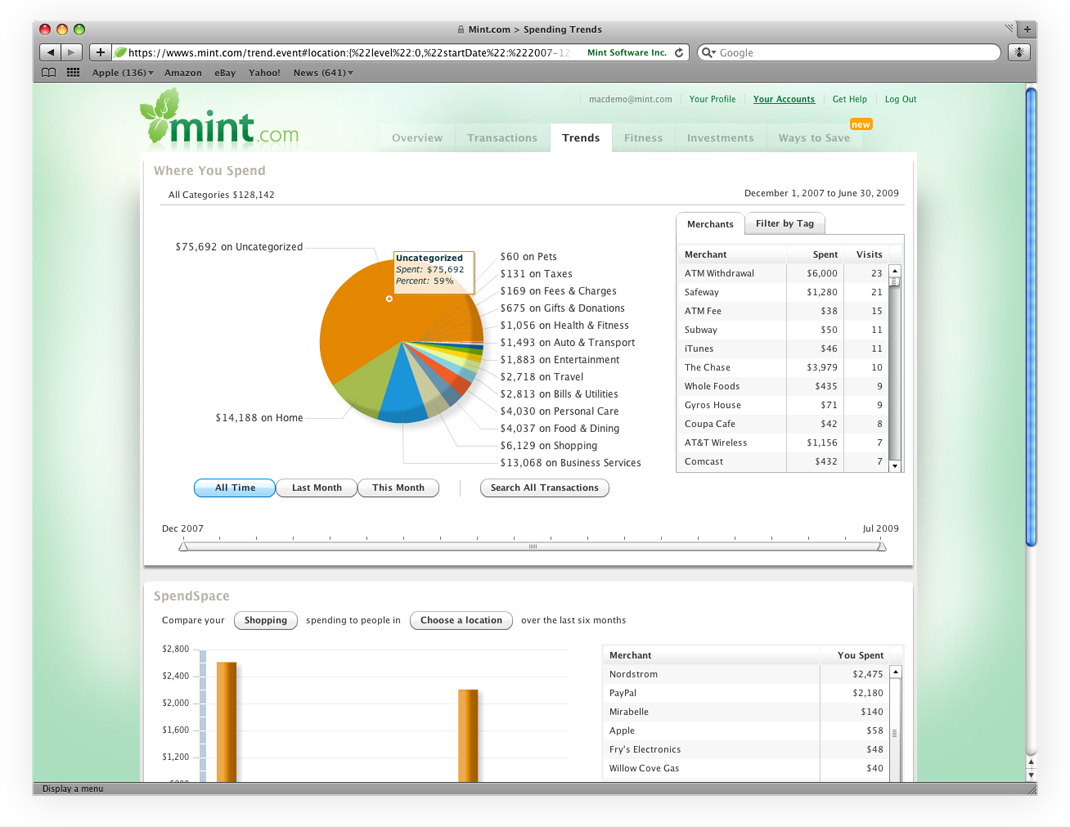

Ability to budget. Sounds daunting but by keeping the budget simple and using online personal financial management tools, budgeting becomes easy. You don’t need an accounting degree to prepare a personal budget. Free personal budgeting software like Mint or free personal investment software like Personal Capital allow you to track your income and spending with very little work on your part. It is also easy to automate your savings and investing with tools like Betterment. You can track things easily but your ability to understand the results of your spending and then to alter your spending are a little bit harder. Leveraging relationships is part of the key to success in this arena as well.

Triggers for budgeting. This is tough. What’s to prompt you to start budgeting if things are going well and you don’t have any major purchases coming up? Tracking your finances is as important as exercising and far easier. It sets you on a path to strengthen relationships by providing you with peace of mind. It’s as easy as creating an account.

Step One: The first step then to change your behavior is to set up a quick meeting with your spouse, significant other, trusted friend or sibling. This meeting is going to be short. You are going to supply food and drinks along with a request. Nothing big. Just some help with accountability. This person must agree to meet with you again in one month to go over your budget. Your spouse will be intrigued and your friend will be confused, but this accountability is essential to beginning the process. Obviously, this must be someone you trust with private, personal information. Oh, and they also need to provide the drinks the following week, just in case you are motivated by something other than fear or desire for acceptance.

Step Two: The next step is to create a couple of different accounts. One to automate your savings and the other to track your spending. I use Capital One 360 for my savings because I can easily a number of different categories within the single account, effectively dividing up my savings into sub-accounts for each goal. This means if I’m saving for next year’s vacation, I can send a portion of my paycheck into my account and then say that some of it is for my upcoming vacation. I like it because it gives me a snapshot of my progress. I use Mint to track my spending mostly because I was an early adopter and already have a lot of data there. Both work well for me though I’ve recently opened accounts at PowerWallet and Betterment.comto see if I prefer their services. The institutions you use are up to you.

Step three: The third step is to start saving. Ideally you’ll put 10% of your income into your savings until you have a nice cash cushion. If all you can manage is $50/paycheck, then do it. But it must be automatically deposited into your account. This can be achieved in two ways. Most companies will offer an automatic deposit program and that’s I how manage my savings. You can also transfer money from your checking to your savings. Betterment will pull money right from your account and plug it into a savings account (downside is you have to deposit $100/month. See my Betterment Review for my details).

Step four: Add goals and emergency plans, then wait and watch. Think about your upcoming year. Odds are that you want to go on vacation, that you’ll need to spend money on car repairs, and that you have at least one other major purchase. Add these big events to your PowerWallet or Mint budget and the start watching your spending. Start accumulating data in your automatic tracking software. You’ll feel empowered as you track your spending and start to see the charts and graphs that create a snapshot of your financial world. Seeing your spending will also enable you to do step five.

Step five: At the end of the month, take a look at a snapshot of the previous month. Look at the broad spending categories and ask yourself if this is a typical month. Look at your net worth and decide if there is anything you can change. Write down the results and get ready for your meeting.

Step six: Report the results over dinner with your friend or spouse.

You did it. It helps to keep this meeting for about three months. After that the exact details of your budget lose some of their importance if you are making changes based on what your budget is telling you. If you are in dire straits, keep this meeting until you are out of debt or have made it through the crisis.

I’ve tried to keep this simple and help change behavior my looking at motivation, ability, and triggers. Your friend is there to help you stay accountable and to help provide the acceptance and love you crave. The software provided the ability. The trigger? Hopefully you’ve already triggered the process by setting up an account and a meeting.

Building budgeting habits is critical to financial well-being. These simple steps will help you get on the path by keeping you accountable and providing some rewards for your work.